Understanding How Written-Off Debts Are Exploited by Fake Debt Collectors

This was confirmed in Van Lynn Developments v Pelias Construction Co Ltd (1968), where Lord Denning stated that “the debtor is entitled to view the sale agreement to ensure that the assignee can give him good discharge under the contract.”

What Happens When a Debt Is Sold

When a debt is sold or transferred to another company, that company must be able to prove they have the legal right to collect it.

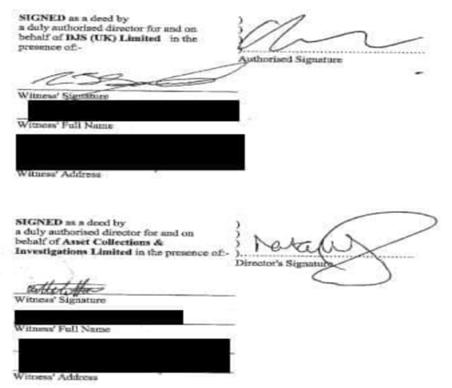

This proof comes in the form of a Deed of Assignment of Debt.

Typically, the Deed of Assignment should be created within seven days of the debt being purchased or the right to collect being transferred.

You have an absolute legal right to request a copy of this document.

Usually, before a Deed of Assignment is shown, you’ll receive a Notice of Assignment — a letter from the new company stating they have bought or are now collecting your debt.

For many people, this is the first letter they receive and often ignore, but it’s important to understand what it really is:

Anyone can send a letter claiming to have bought a debt, but unless they can provide a valid Deed of Assignment, they have no enforceable right to collect that debt.

A Deed of Assignment is a legal document that transfers ownership of a debt from the original creditor to a third party (the debt purchaser).

For it to be legally valid, it must:

If these requirements are not met, the document is not legally valid, and the debt purchaser cannot lawfully enforce the debt in their own name.

In practice, debt collection companies rarely provide the Deed of Assignment when requested.

That’s often because:

Always:

This website has been created by former MatrixFreedom staff and members to support individuals who have experienced financial hardship in connection with Iain Clifford and the Sovereign Reserve Program.

The information provided here is for educational and informational purposes only and is completely free to access.

We also operate a separate website, MatrixFreedom Exposed, which documents the full history of events, including misleading claims and business practices, and outlines the steps being taken to prevent further harm.

👉 For more information, please visit: www.matrixfreedomexposed.info